The component market in June 2026 showed a K-shaped divergence, with tight supply and demand for AI servers and high-end automotive applications, while traditional consumer electronics recovery remained weak, entering a structural long-term shortage cycle.

Passive components and memory chips simultaneously launched the second round of price increases. The surge in AI computing equipment consumption has consumed a large amount of wafer capacity, and the sharp rise in automotive-grade memory prices has forced car manufacturers to adjust prices. Combined with sudden production damage at overseas factories, the 800 billion scale domestic substitution market has entered an accelerated release window.

June Component Industry Overview

(1) Passive Component Leaders (MLCC/Resistors/Film Capacitors)

① Murata (Global MLCC Leader)

On June 11, Murata officially issued a price adjustment notice to its agents, effective July 1: AI servers and 800V automotive-grade MLCCs saw price increases of 10%-40%. High-end product lead times have been extended to 16-24 weeks, and the company has stopped accepting orders for some low-end consumer products, shifting all capacity toward high-end models related to AI computing power.

② Samsung Electro-Mechanics

On June 1, Samsung Electro-Mechanics followed Murata in implementing price hikes. The X5 series MLCCs have already seen price increases of 20%-50% and are no longer accepting new orders. Production lines have fully shifted to produce X6S and higher AI-specific models. Starting July 1, the original factory will initiate comprehensive price adjustments with core direct customers.

③ Yageo (Taiwanese MLCC Leader)

On June 22, Yageo initiated the second round of channel price adjustments, with a general MLCC price increase of 20%. Popular models like 104 and 105 saw price increases exceeding 40%.

④ Huasheng (Second-largest chip resistor manufacturer globally)

On June 21, Huasheng released an official price increase notice, raising prices across the entire range of 0201-1206 chip resistors, with old prices invalidated and new negotiations required. A single price increase of 20%-30% was implemented. However, due to Fenghua High-tech announcing a much higher increase than Huasheng's internal plan, Huasheng made a significant move before the Dragon Boat Festival to withdraw its price list and request re-negotiation. New prices will take effect on July 1, covering general thick-film resistors, AI and automotive alloy sampling resistors.

⑤ Fenghua High-tech (Mainland China's Leading MLCC Manufacturer)

In June, Fenghua High-tech's new high-performance capacitor base was fully operational, with a monthly capacity of 6.5 billion units, and 100% of the new capacity is allocated to AI servers and new energy vehicle manufacturers. In June, the channel also raised the price of domestic MLCCs by approximately 20%-30%, with orders already scheduled through 2027.

⑥ Far East Electronic (Leader in Film Capacitors)

Far East Electronic's 800V high-voltage film capacitors have entered the power supply supply chain of NVIDIA GB200/GB300. Panasonic and KEMET also raised the prices of similar specifications of film capacitors in June, with price increases of 30%-50%.

(2) Memory Chip Leaders

① Micron

Micron released its Q3 fiscal year 2026 financial report: Revenue of $41.46 billion, up 346% year-over-year, net profit of $28.24 billion, gross margin of 84.9%; Micron has secured a $22 billion commitment for long-term memory chip procurement.

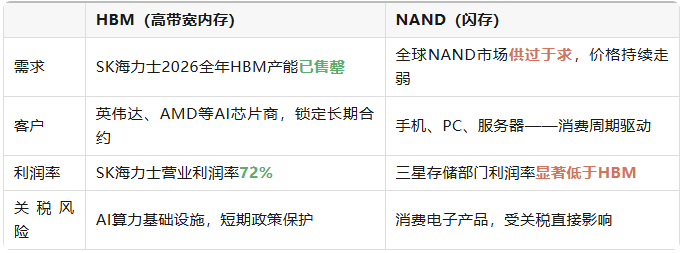

② Samsung and SK Hynix

Data shows that Samsung and SK Hynix together account for 67% of the global DRAM market and 47% of the NAND market.

All DRAM and NAND capacities for 2026 have been sold out, with channel inventory at only 2-4 weeks (healthy range is 8-12 weeks). Priority is given to HBM computing storage supply, while general storage spot prices continue to rise.

③ Biwin Storage (Leading Domestic Storage Module Manufacturer)

Biwin Storage disclosed its first-quarter report data: net profit of 2.899 billion yuan, up 1567.85% year-over-year; AI server storage module orders continue to rise month-over-month, with advanced packaging capacity operating at full capacity.

(3) Power Semiconductor / Analog IC Leaders

① Yangjie Technology

On June 26, Yangjie Technology officially announced a price increase: all products will be increased by 10%-15% starting July 1. This is the company's second price adjustment this year. In late March, it adjusted new order prices via dealer channels, mainly affecting certain products; however, the latest price increase will cover all product categories.

② Infineon, Texas Instruments, STMicroelectronics

In June, these companies sent price adjustment notifications to their agents, with price increases in July. AI server PMICs and high-voltage power devices saw price increases of 15%-25%, while automotive and industrial control devices saw price increases of 10%-15%, while consumer-level analog chips maintained stable pricing.

③ Stacc (Standex Semiconductor), Silan Microelectronics

Stacc delivered large quantities of automotive-grade IGBT modules to European Tier 1 suppliers, and its 6-inch SiC MOSFET production line rapidly ramped up. Silan Microelectronics will raise prices by at least 15% starting July 1, joining a new round of price hikes with nearly 20 global power semiconductor companies.

(4) PCB / Packaging Substrate Leaders

- Shennan Circuit: On June 23, the company announced an investment of 6 billion yuan for the construction of a packaging substrate production base in Guangzhou. After full operation, the project is expected to have a capacity of approximately 200 million FC-BGA and 3 million panel RF/FC-CSP organic packaging substrates.

- On June 23, the PCB market circulated the rumor that "NVIDIA required PCB manufacturers to reduce prices by 10%." Currently, NVIDIA's investor relations department has clarified - the claim that NVIDIA enforced a 10% price cut is completely false. There is no uniform policy for a one-size-fits-all price reduction, and annual framework orders still follow the original commercial pricing.

Deep Analysis of June Component Cycles

(1) Supply and Demand Divergence

① High-Performance Shortage Sectors (Computing, Automotive, Energy Storage)

Five categories including high-capacity MLCC, HBM memory, high-voltage film capacitors, server power components, and high-end packaging substrates have formed a hard supply gap: factory utilization rates have exceeded 90%, expansion cycles are long, and equipment delivery is restricted. Order production schedules are generally 6-12 months, and factories prioritize securing long-term prepayment agreements with cloud vendors and top-tier automotive clients. Small terminals and traders face increasing difficulty in obtaining supplies.

② Weak Recovery Sectors (Mobile Phones, Laptops, Traditional Home Appliances)

Low-end general resistors and capacitors, ordinary NOR Flash, and consumer-grade MCUs have seen weak demand. Factories actively reduced mid-to-low-end production lines, switching to high-margin AI and automotive-grade models. Channel inventory slowly depletes, with prices rising slightly, but without shortage pressure.

(2) Price Cycle

- The MLCC shortage in 2018 was caused solely by Japanese contraction of consumer capacity. After inventory recovery, prices quickly declined. In 2026, the situation is driven by long-term AI computing infrastructure and the dual rigid demands of new energy vehicles' intelligence, with a multiple increase in per-unit component usage, and demand growth is sustainable;

- Raw materials such as precious metals, ceramic powders, copper, and tin continue to rise in cost, and factories have exhausted their cost-reduction space. Price hikes are a result of cost rigidity transmission, not short-term speculation by channels;

- There is a 2-3-year time lag in the expansion of 8-inch mature wafer and MLCC sintering equipment capacity globally. In the short term, there is no large-scale new supply to offset the demand gap.

(3) Current Status of Agent Channels

- Factories have tightened supply distribution, implementing three controls: monthly rolling forecasts, long-term prepayment agreements, and quota-based supply. Small traders without long-term cooperation agreements find it difficult to obtain stable sources. Shunhai Technology holds official first-level authorization from multiple well-known manufacturers and has reached deep strategic partnerships with factories, possessing stable quota sourcing capabilities and direct factory supply channels.

- Channel prices fluctuate daily, with the gap between spot and contract prices continuing to widen. The willingness to stockpile scarce part numbers has increased, but factory control over supply suppresses irrational speculation. Faced with industry price fluctuations and unstable supply of scarce parts, Shunhai Technology relies on its complete spot inventory system and mature supply chain management capabilities, maintaining a full range of conventional and scarce components in stock, strictly controlling source quality.

- The demand for domestic substitution has exploded, with end customers actively diverting orders to mainland manufacturers, resulting in a continuous increase in the shipment of domestic components. Aligning with the trend of domestic substitution, Shunhai Technology has built a complete domestic component supply chain, integrating resources from multiple high-quality domestic manufacturers, providing one-stop solutions for customer needs for domestic substitution and multi-category procurement.

Final Words

The component supply-demand gap driven by AI computing power continues to expand. After the new price hike takes effect on July 1, the industry's high-price, long-lead-time situation will persist. The convergence of upstream costs, overseas production disruptions, and downstream high-end demand will continue to accelerate the pace of domestic component substitution. Upstream and downstream enterprises in the industrial chain need to prepare in advance, expand supply channels, and smoothly cope with this cycle fluctuation.