Capacitors are known as the "electronic circuit's RAM". They support filtering, energy storage, voltage stabilization, and buffering. Although small in size, they play a vital role in the supply chain.

For a long time, capacitors have been considered as "supporting actors" in the electronics industry: each costs just a few cents, and among the three basic components of resistors, capacitors, and inductors, it has the least presence. However, in 2026, the industry's traditional perception was overturned.

Currently, three major industry trends - the reconfiguration of components in AI servers' GB300 cabinets, the shortage of high-end capacitors, and the acceleration of domestic substitution - have transformed capacitors from unremarkable auxiliary components into the underlying hardware barrier that supports AI computing power and the stable operation of the new energy industry.

Key Points: Currently, all five types of capacitors are experiencing simultaneous supply-demand gaps, but the reasons for the shortages vary. MLCC shortages stem from insufficient high-end capacity, supercapacitor shortages come from the increased demand for full standardization across the industry, tantalum capacitors face dual constraints from raw materials and certification, and film and aluminum electrolytic capacitors have shortcomings in high-voltage new materials. The supply and demand structure determines pricing power, and scarce categories control price leadership.

Analysis of the Industrial Structure and Incremental Logic of Five Capacitor Categories

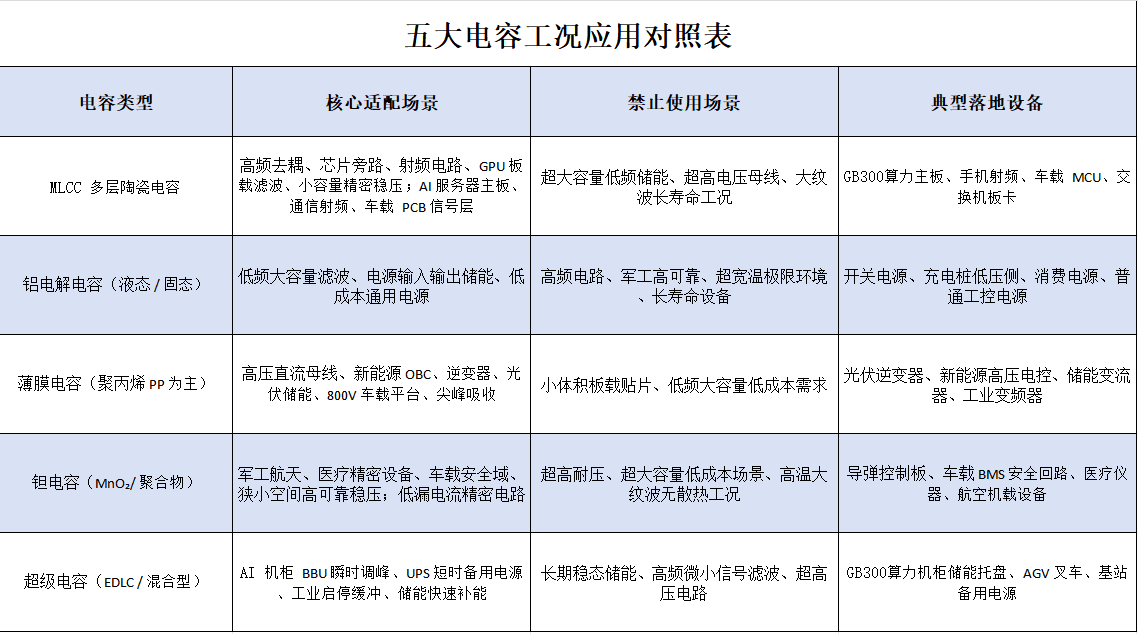

1. MLCC Capacitors: AI Servers Emptying Global High-End Capacity, Domestic Substitution Reaches a Profitability Turning Point

MLCC is the most widely used basic capacitor in electronic devices, and AI computing power hardware has completely reshaped the industry's demand structure. A regular smartphone requires only hundreds of MLCCs, while traditional servers require thousands, whereas NVIDIA's GB300 AI server requires 30,000 MLCCs per machine, up to 440,000 per cabinet. Next-generation VR200 platform demand will increase by 30%, making AI the core growth engine for high-end MLCCs.

Ceramic Capacitor

The supply side faces rigid bottlenecks. The construction of high-end MLCC production lines and the yield ramp-up cycle can last 18-24 months, with single-line investment reaching tens of millions of yuan, making capacity expansion extremely difficult. Currently, the utilization rate of high-end production lines of Japanese and South Korean leaders such as Murata and Samsung Electro-Mechanics exceeds 90%, and their order volumes are double the capacity. The industry's price increase cycle has fully started.

Under the tense supply and demand structure, domestic substitution is accelerating. Fenghua High Tech and Sanhuan Group have achieved mass production of high-end MLCCs, and Guoci Material's ceramic powder has entered the global forefront. China has built a complete industrial chain from raw materials to terminal components. The current situation of Japanese and South Korean price increases and delivery delays continues to drive downstream manufacturers to adopt domestic products, marking the industry's transition from the "available phase" of domestic substitution to the "profitable replacement" stage.

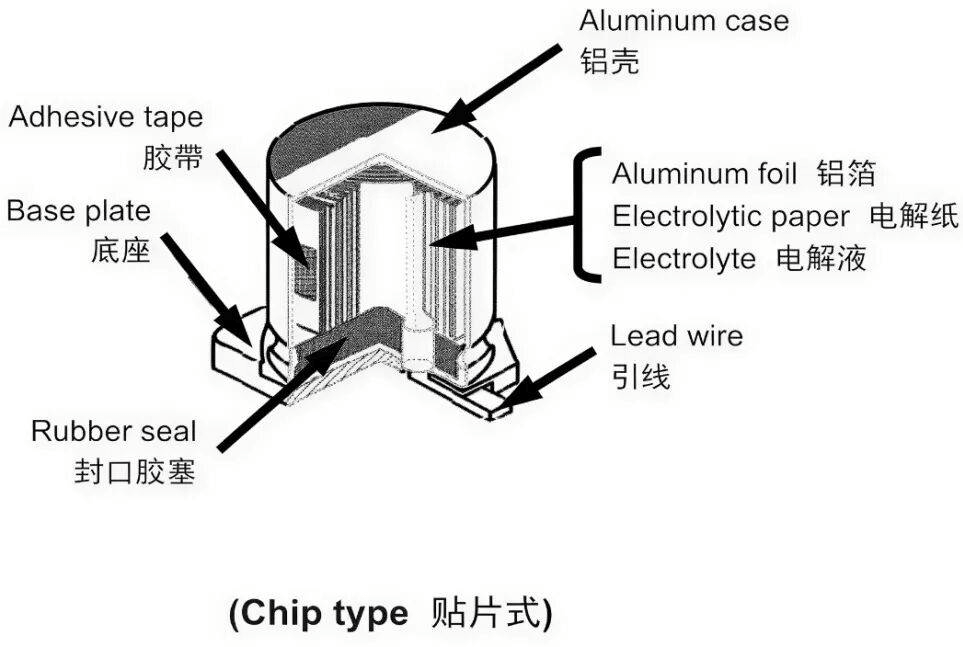

2. Aluminum Electrolytic Capacitors: High-Voltage Demand Is Irreplaceable, Core Value Lies in Upstream Materials

Aluminum electrolytic capacitors are the only type capable of achieving low-cost high-voltage output of 450V-600V, making them essential components for AI server power supplies and new energy vehicle 800V high-voltage platforms. The sector has strong barriers.

For a long time, the global high-end market has been monopolized by Japanese Nippon Chemi-Con and Ruby. However, Japanese manufacturers have been continuously reducing mid-to-low-end capacity, leading to a steady decline in industry supply. Coupled with AI computing power construction and the upgrade of new energy vehicle high-voltage platforms, global demand for high-voltage aluminum electrolytic capacitors has reached an all-time high.

The core competitiveness of this category is not in capacitor cell manufacturing, but in upstream materials such as electrode foil and electrolytic paper, where anode electrode foil accounts for 30%-60% of the finished product cost. Haisen Shares, as a global leader in electrode foil, is expected to increase its share after new capacity comes online. Kain Shares has a global market share of over 30% in electrolytic paper, firmly holding the top position in the industry.

The higher the self-sufficiency rate of upstream materials, the stronger the cost control and price transmission capabilities. The core profits of the industry concentrate in the upstream key material segments.

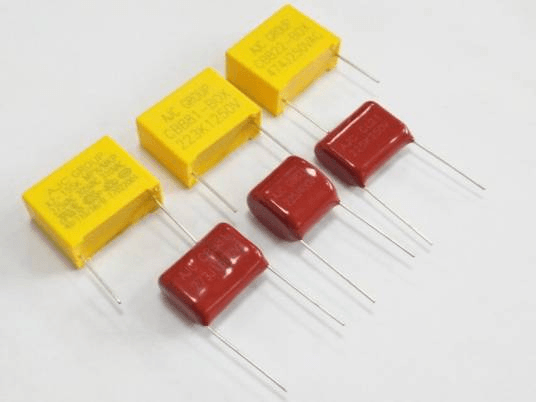

3. Film Capacitors: Core Configuration for New Energy, Certification Barriers Build a Moat

Film capacitors, with their high-voltage tolerance, long lifespan, and self-healing properties, perfectly match the new energy industry upgrade. The iteration of new energy vehicles from 400V to 800V/1000V high-voltage platforms and the upgrade of photovoltaic systems from 1000V to 1500V significantly increase the number of capacitors per vehicle and per unit, driving continuous growth in industry demand.

Domestic leader Faraday Electronics has a significant monopoly advantage, with a global market share of over 30% in new energy vehicle supporting capacitors and nearly 70% in photovoltaic storage fields, maintaining a gross profit margin more than 10% higher than competitors for a long time.

The core barrier of the film capacitor industry is not the scale of production capacity, but the strict industry qualification certification, which makes the rare access rights to high-end scenarios the core confidence for long-term leadership.

4. Tantalum Electrolytic Capacitors: Resource + Certification Dual Barriers, AI Opens New Growth

Tantalum capacitors are small in size, have low leakage current, and maintain stable performance under extreme temperature conditions, making them irreplaceable components in military aerospace and high-end computing equipment. They are widely used in core equipment such as military radar and missile guidance. Starting from 2026, AI servers became the largest incremental source, and under the stringent high-temperature working conditions of GPU power modules, tantalum capacitors outperform MLCCs, driving rapid industry expansion due to computing power demand.

Tantalum Capacitor

The industry has two hard-core barriers. The upstream tantalum ore is highly concentrated in the Democratic Republic of the Congo and Rwanda, and geopolitical conflicts have caused tightness in the mineral sources and rising raw material prices, forming a natural resource barrier. Downstream military and computing power sectors require long and high-barrier certification cycles, building a time barrier.

In the industry, Dongfang Tantalum controls core tantalum powder and wire resources, while Hongda Electronics and Zhenhua Technology focus on the military field, with deep qualifications. Their civilian products have already been supplied in bulk to domestic AI servers and successfully entered overseas top computing power supply chains.

5. Supercapacitors: From Optional to Standard, Becoming the Largest Supply-Demand Gap Segment

Supercapacitors have ultra-large energy storage capacity, microsecond-level response speed, and tens of thousands of cycle life. Previously, they were only applied in traditional scenarios such as wind turbine pitch control and grid frequency modulation. In 2026, the industry reached a turning point, with NVIDIA's GB300 platform upgrading supercapacitors from optional to standard, with over 300 units per cabinet. Annual new demand far exceeds global existing capacity, making it the most acute and certain segment among the five capacitors.

As the industry configuration standards improve, pricing power is concentrated in leading companies with mass production capabilities. Jianghai Shares' products have been perfectly adapted to the GB300 solution and are one of the few manufacturers with both R&D and system integration capabilities. At the same time, companies like Dongyang Guang and Xichen Carbon Energy are accelerating their layout to seize the industry's high-temperature growth opportunities.

The Five Capacitor Selection Boundaries Are Clearly Defined

Different capacitor materials and structures determine their inherent application scenarios, and there is no universal alternative relationship. The core selection criteria are: choose MLCC for high-frequency decoupling, film capacitors for high-voltage energy storage, aluminum electrolytic capacitors for large-capacity and low-cost, tantalum for military-grade reliability, and supercapacitors for instantaneous voltage stabilization in computing cabinets.

Comparison Table of Working Conditions and Applications for Five Capacitors

Final Words

As AI computing hardware continues to iterate and new energy high-voltage platforms become widespread, the high-growth cycle of the five capacitor segments will continue.